Why an Artwork Bought for $100 at a Garage Sale Could Fetch $1 Million at Auction

A market where price never tells the whole story In the art market, one of the most persistent misconceptions is the idea that an object has “a single value.” In reality, things are far more nuanced: the same asset can have radically different prices depending on where and how it is sold.

This is where the stories that frequently circulate in the public space come from—objects bought for symbolic amounts and later resold for millions. Beyond the fascination of such cases, the mechanism is perfectly explainable from an economic standpoint: the art market is not a single, unified market, but rather a set of parallel markets, each with its own rules, different levels of risk, and varying degrees of information.

An artwork does not have a single value, but multiple values simultaneously In professional valuation, the concept of “value” is neither unique nor absolute. Instead, there are several types of value, defined according to the purpose of the valuation.

An asset may have one value for taxation, another for insurance, another for quick sale, and yet another for orderly market transactions. These differences are not theoretical—they reflect distinct economic realities: the same object sold under time pressure will yield a different financial result than the same object sold after a period of marketing and exposure.

This plurality of values is essential for understanding why, in art, price is never solely the result of the object itself, but of the context in which it is introduced to the market.

The central issue: the market in which the object is sold One of the most important variables in price formation is the market in which the transaction takes place. In valuation, this is known as the “relevant market”—that segment of the market where the asset is typically traded.

To understand this intuitively, one can compare two situations: purchasing an item from a specialized store, with warranty, invoice, and full transparency, versus buying the same item from an informal platform, where information is limited and risk is largely transferred to the buyer. Although the object is identical, the price differs because both risk and information differ.

In the cultural goods market, this difference manifests on a much larger scale and generates three main market tiers.

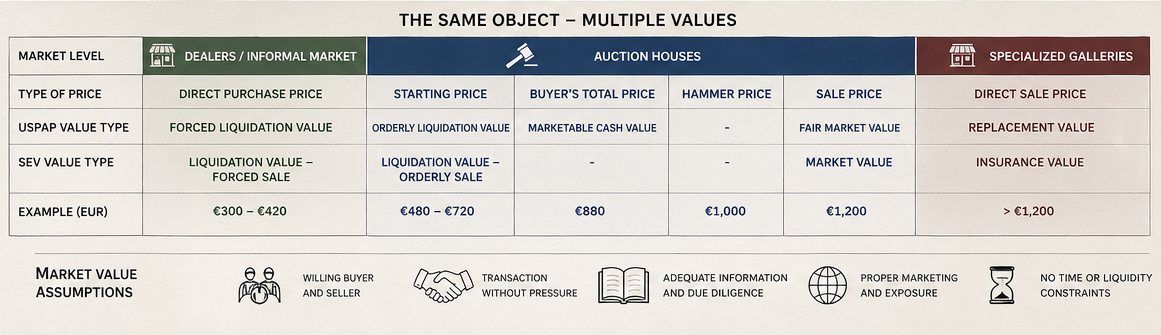

Three parallel markets for the same type of asset At the base of the art ecosystem, there are, in practice, three distinct market levels, each with its own economic logic.

The first is the market of small dealers—fairs, informal sales, general online platforms, or “garage sales.” This segment carries the highest level of uncertainty. Information about authenticity is limited or nonexistent, guarantees are minimal, and risk is borne primarily by the buyer. Naturally, this pushes prices downward, even if transaction volumes are high.

At the opposite end is the market of galleries and specialized shops. Here, selection is strict, clientele is well-defined, and the sales process is often consultative, almost experiential. Information is detailed, guarantees are strong, and marketing is targeted. As a result, prices are generally the highest in the market.

Between these two extremes lies the auction house market, probably the most visible to the public. Here, the process is transparent, competition is direct, and the final price results from the interaction between supply and demand. Auction houses invest in authentication, promotion, and exposure, reducing buyer risk and, implicitly, supporting higher price levels.

Why the same object can “migrate” between radically different prices Price differences arise precisely because the same asset can be introduced into different markets, with varying levels of efficiency and risk.

An incorrectly identified object, sold in an informal context, may trade at a very low price. If the same object is later authenticated, promoted, and introduced into an auction, it may reach a value tens or even hundreds of times higher.

Conversely, an object typically traded through auctions may achieve a lower price if sold quickly, without exposure, in an informal setting.

The difference lies not in the object itself, but in information, trust, and market structure.

What “market value” actually means In valuation, market value is defined as: “the estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm’s length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently, and without compulsion.”

This definition includes four essential conditions: the existence of willing parties, a transaction free of pressure, an adequate level of information, and proper market exposure.

An important element, often overlooked in public perception, is that market value assumes the absence of time or liquidity constraints. In other words, it is not a “quick sale” value, but one of economic equilibrium.

Auctions: the closest mechanism to the theoretical market In practice, auction houses are the closest functional model to the concept of market value. The process is standardized: an asset is introduced with a starting price, participants bid incrementally, and the item is awarded to the highest bidder.

However, this final price—known as the hammer price—is only part of the economic equation. In reality, the transaction includes commissions for both buyer and seller, which substantially alter the effective economic value of the operation.

In practice, these commissions can reach 20–25%, meaning that the amount paid by the buyer and the amount received by the seller differ significantly from the hammer price.

Thus, for the same transaction, multiple values may coexist simultaneously: the hammer price, the total price paid by the buyer, and the net amount received by the seller.

Why the same transaction generates multiple “values” This distinction is important for understanding the art market, because depending on the valuation standards used, market value may include or exclude commissions.

In certain international standards, including U.S. tax practice, market value is interpreted as including buyer-incurred costs, which significantly affects the final level of value.

This technical nuance explains why, at times, the same artwork may have different values in different valuation reports, without any of them being incorrect.

Beyond the reference market: other types of prices In addition to market value, other price levels also exist in practice. The starting price in auctions, for example, often reflects a liquidation value—the minimum acceptable level in an orderly sale.

This may be significantly lower than market value, sometimes even half of it.

By contrast, in galleries or specialized retail environments, prices may exceed market levels, as they include services, curation, access, and the purchasing experience. In some cases, these prices are comparable to insurance values, where immediate availability is more important than price optimization.

The price landscape for an artwork could be illustrated as follow

Conclusion: value belongs not only to the object, but to the market in which it circulates In the valuation of art assets, the correct question is not “how much is the object worth?” but rather “in which market and under what conditions is it being valued?”

The same artwork may be undervalued in an informal context, fairly valued in an auction, and overvalued in a premium commercial setting. These differences are not anomalies, but the natural result of different markets operating simultaneously.

For investors, collectors, and institutions, this distinction is essential. And for valuers, the stake is not merely setting a price, but correctly identifying the relevant market—the only element capable of anchoring value within a coherent economic reality.